Cristina 1 review | February 16, 2023

General Review

(Edited)

Reply

Share

Helpful? (0) You found this review helpful

Post reply

LoanBuilder is a loan service by popular payment processor PayPal. Loans obtained from LoanBuilder are facilitated by Swift Financial.

LoanBuilder offers your company the short-term capital it needs to bridge the gap between large contracts, buy new equipment, and more.

Aimed at small and medium-sized businesses, it offers loans up to $500,000 with flexible weekly payment terms that allow your business to pay off the balance over time.

Although similar to other online lenders, LoanBuilder is a bit quicker and easier to qualify for, which is why it’s popular among businesses in the U.S.

So, how does a loan from LoanBuilder work and how can you tell if it’s the right option for your company? We’ll explore these topics and more below.

At Financer.com, all lenders go through a thorough research and review process. Here’s how we rate LoanBuilder:

| Category | Rating |

|---|---|

| Affordability | ⭐⭐⭐⭐ |

| Application process | ⭐⭐⭐⭐ |

| Loan terms | ⭐⭐⭐⭐ |

| Transparency | ⭐⭐⭐⭐ |

| Customer support | ⭐⭐⭐ |

| Overall | ⭐⭐⭐⭐ |

Want to skip the details? Jump to our final verdict here.

LoanBuilder offers businesses short-term loans to help them continue operating while generating stable revenue.

Here’s a quick summary of LoanBuilder:

| Overview | Features |

|---|---|

| Loan type: | Business loans |

| Loan amount: | Up to $500,000 |

| Loan term: | Up to 52 weeks |

| APR: | From 2.9% to 18.72% |

| Min. credit score: | 620 |

| Monthly fees: | None |

| Payout time: | One business day |

| Weekend payout: | No |

| Requirements: | At least 18 years old U.S. citizen No active bankruptcy filings Credit score of 620+ Business must be registered with the Secretary of State |

It gives businesses loans from $5,000 to $500,000 to buy equipment, pay salaries, buy a new building, and more while allowing the company to make regular weekly payments.

Because payments are made weekly, businesses can easily budget for them according to their cash flow and put their funds to work immediately.

LoanBuilder also offers businesses loans as small as $5,000, so these loans can even cover small purchases for your business.

What’s more, with weekly payments available, planning and paying off your debt in a shorter period of time is possible.

PayPal Business Loans and LoanBuilder are the same. In fact, LoanBuilder was formally known as PayPal Business Loans, and while the original loan product allowed customers to repay with monthly payments, LoanBuilder allows borrowers to repay their loans in weekly payments.

Another option is PayPal Working Capital, which offers business loans based on your PayPal account history. You repay with a share of your PayPal sales.

PayPal Working Capital has loans from $1,000 to $150,000 for first-time borrowers and up to $200,000 for repeat borrowers.

LoanBuilder has a very easy application process that takes a few minutes. You’ll get your loan offer right away.

Another benefit of LoanBuilder is that there are no fees unless you make a late payment, in which case there is a $20 fee due.

Only short-term loans

High minimum loan amount of $5,000

No benefit to repaying a loan early

Although LoanBuilder is ideal for larger businesses, the repayment terms are up to 52 weeks. If you need a long-term loan it might not be the best option.

PayPal LoanBuilder loans are for businesses only. More specifically, for established businesses with consistent, documented revenue.

To get a LoanBuilder loan, you must have been in business for at least nine months and have at least $42,000 in yearly revenue.

You must also have no active bankruptcy filings, a minimum credit score of 620, and the business must be located in the U.S.

Your business also must be registered with the Secretary of State.

On top of all those regulations, there are select industries and business types that are not eligible at all.

There is a personal guarantee attached to PayPal LoanBuilder loans. This means you would be financially responsible for repaying the loan if the business defaults.

LoanBuilder APRs range from 2.9% to 18.72% with 6% to 19% fixed interest.

There are no origination fees, no prepayment fees, and no maintenance fees. However, there is a $20 returned payment fee.

You repay the loan weekly, and the terms range from 13 to 52 weeks.

Your interest rate will vary greatly depending on your creditworthiness, and a loan consultant will go over this with you if you’re approved.

Every week, LoanBuilder will deduct a fixed amount from your business bank account via an ACH (automated clearing house).

Should you decide to pay off your LoanBuilder loan early, keep in mind that all the fees are calculated at the time of loan funding, so this is one of those rare instances where there is no real benefit to paying off early.

PayPal participated in the Paycheck Protection Program (PPP) through WebBank, Member FDIC.

However, as the SBA announced in May 2021 that PPP loan funding had been depleted, LoanBuilder PPP loan applications are no longer accepted.

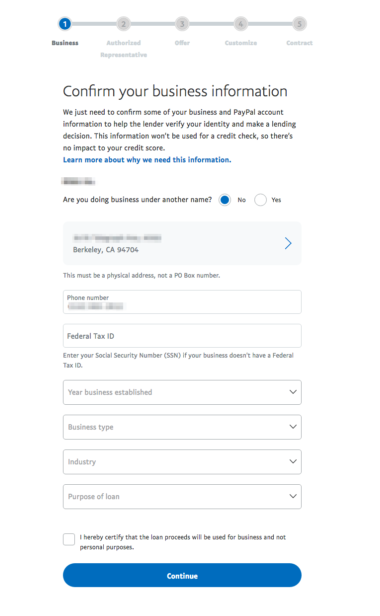

During the first step of the application process, you’ll need to provide your contact info, which includes your name, email address, phone number, and intended use of the loan proceeds.

Next, you’ll need to provide your personal information, including your home address and telephone numbers. You’ll also have to provide your business address and telephone numbers.

When it comes to business details, you’ll supply relevant information, such as your business entity type, trade name or DBA, state of incorporation, annual business revenue, business start date, number of full-time employees, and business industry and sub-industry.

Once you submit your application, LoanBuilder will let you know whether you qualify to continue with the process.

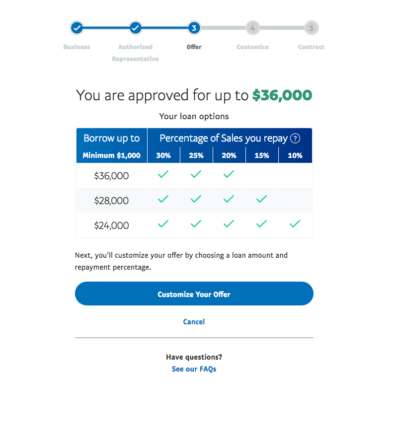

If preapproved, you will receive estimated rates and fees and you can customize your loan amount and term length. Once determined, you can complete a full application.

You will need to submit documentation, which can include business bank accounts. LoanBuilder will also perform a hard check on your credit profile which may temporarily reduce your credit score.

If approved, you’ll electronically sign your contract before receiving your funds.

LoanBuilder is extremely transparent about its fees. It’s a reputable lending platform built on PayPal’s reputation, which has been around since 1998.

Another benefit is the LoanBuilder Configuration Tool which helps you understand what you will be paying for your loan. You can adjust the amount and term length to get a clear understanding of what to expect.

If you use PayPal to process business payments, you can use the PayPal Working Capital Loan or the PayPal Suite of processing tools.

Before being acquired by PayPal in 2017, Swift Financial already had a solid reputation for top-notch customer service. This standard remains today.

The support team is available Mondays to Fridays from 9 am to 8 pm ET and on Saturdays from 11 am to 3 pm ET. You can reach the customer support team via phone at 1-800-347-5626.

LoanBuilder is connected to one of the most powerful financial services companies in the world, PayPal, so you know it is a legitimate business lender.

Read more LoanBuilder reviews below or add your own.

Here’s a list of alternatives to LoanBuilde and how they compare:

| Lender | Reviews | Loan Amount | APR | Max. Loan Term |

|---|---|---|---|---|

| Fundera | View | Up to $5 million | Up to 36% | Up to 6 years |

| Uplyft Capital | View | Up to $500,000 | 1.12 – 1.4 factor rate | 2 – 2 months |

| Nav | View | Up to $5 million | Vary by lender | Vary by lender |

| Lendio | View | Up to $5 million | Up to 24% | Vary by lender |

LoanBuilder gets 4.3 out of 5 stars on Trustpilot, with users generally feeling happy about the service:

LoanBuilder seems to respond to negative reviews and sort out issues as they arise, making them responsive lenders.

Read more reviews on Financer.com from verified users below.

Have you used LoanBuilder before? Leave your review now.

Hi Jerry.

Can you provide more details on the transaction? I am contacted by them for a small biz loan.

Thanks,

D

Rate & Review LoanBuilder

Your rate for this company. Edit Rate

Take a minute to write a review!

Share your experience and help others to choose the right company.

Pros

Cons

Visit their official website and learn more about LoanBuilder

Or sign in with email

The username or password is incorrect.

Authentication Code:

Thank you for choosing

Share your experience and help others to choose the right company.

This website uses cookies among other user tracking and analytics tools. Cookie information is stored in your browser and performs functions such as recognizing you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful. Cookies may also be used for other marketing and advertising purposes, or for other important business analytics and operations.

To use our website you need to agree to our Terms and Conditions and Privacy Policy. To find more about the legal terms that govern your use of our website, please read our Terms and Conditions here.To find more about your privacy when using our website, and to see a more detailed list for the purpose of our cookies, how we use them and how you may disable them, please read our Privacy Policy here.