(Edited)

UpsidesSoFi has been my financial ally, and the experience has been nothing short of exceptional. The platform seamlessly combines cutting-edge technology with a personal touch.

Downsidesgreat

Join the weekly Finance Stacks newsletter for expert advice on stacking extra cash.

If you are looking for a large loan and you have an excellent credit history, then SoFi may be the ideal lender for you.

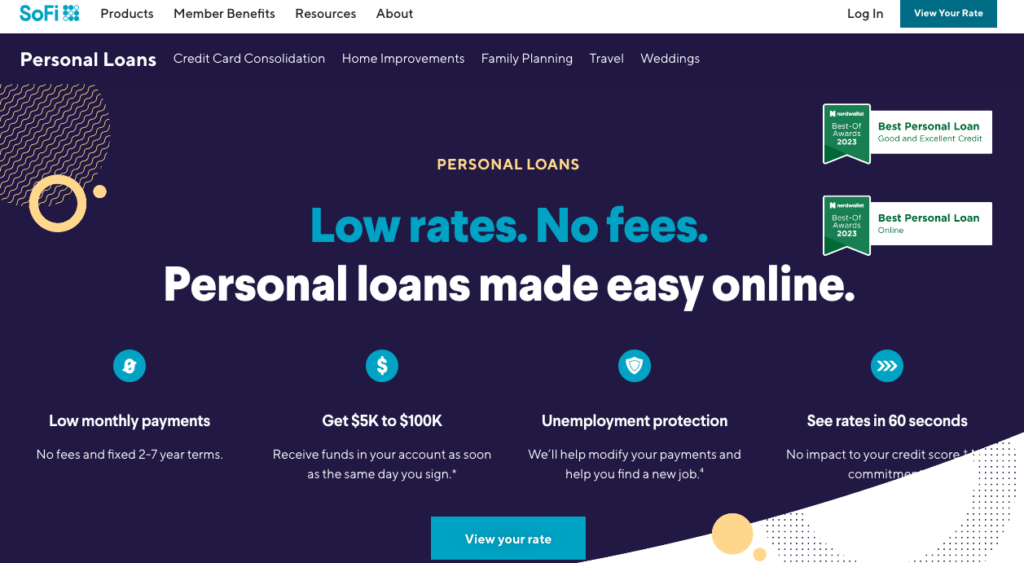

SoFi offers an array of loan packages, from personal loans to mortgages as well as mortgage refinancing. Loans are available from $5,000 to $100,000 with rates starting at 8.99% APR*.

Loan terms range from two to seven years and the minimum credit requirement is 680.

SoFi loans are available in all US states except Mississippi.

At Financer.com, all lenders go through a thorough research and review process. Here’s how we rate SoFi:

| Category | Rating |

|---|---|

| Affordability | ⭐⭐⭐⭐ |

| Application process | ⭐⭐⭐⭐ |

| Loan terms | ⭐⭐⭐⭐ |

| Transparency | ⭐⭐⭐⭐ |

| Customer support | ⭐⭐⭐⭐⭐ |

| Overall | ⭐⭐⭐⭐ |

Want to skip the details? Jump to our final verdict here.

SoFi – or Social Finance, Inc. – launched in 2011 offering student loan refinancing for Stanford alumni. The company has since expanded its offering into other categories such as mortgage loans and auto loan refinancing.

SoFi offers perks to customers such as estate planning, career coaching, and financial planning. The company uses its coaching and planning services to help its customers stay on top of their finances.

SoFi loans range from $5,000 to $100,000 and are available in all US states except Mississippi.

In states like Massachusetts, Arizona, and New Hampshire, the minimum loan amount is $10,001 while the baseline is $15,001 in Kentucky.

Here’s a quick summary of SoFi:

| Overview | Features |

|---|---|

| Loan type: | Personal loans, mortgage loans, auto loan refinancing |

| Loan amount: | $5,000 to $100,000 |

| Loan term: | Up to 7 years |

| APR: | 8.99% – 25.81% |

| Min. credit score: | 680 |

| Monthly fees: | None |

| Payout time: | 1-3 days |

| Weekend payout: | No |

| Requirements: | At least 18 years old U.S. citizen, permanent resident, or visa holder Live in an eligible state Good credit |

SoFi’s APRs are consistent with lenders offering credit to borrowers with excellent credit. They also offer rate discounts for autopayments and all loan rates and terms are disclosed on their website.

Prequalifying for a SoFi loan requires a soft credit check which means your credit score won’t be affected until you accept the offer.

Want to find out more about the full range of offerings? Read our SoFi review below or view SoFi reviews from customers.

Here are some of the pros and cons of SoFi as a lender:

SoFi personal loans are aimed at borrowers who have a good credit history and a strong cash flow. Since many online lenders cap personal loans at around $40,000, SoFi is the ideal lender for borrowers looking for a huge online loan.

SoFi offers competitive interest rates, especially if you have strong credit. You’ll also be eligible for a 0.25% rate discount if you set up AutoPay.

People with less-than-fair credit may have a tough time qualifying

$5,000 minimum loan amount (may be higher in some states)

SoFi loans cannot be used to buy securities, real estate, investments, or used for business purposes. Loans can also not be used to cover postsecondary educational expenses.

SoFi loans are ideal for borrowers with good to excellent credit looking for a large loan with flexible repayment terms and zero fees.

To qualify for a SoFi loan, you have to meet the following requirements:

SoFi may be a good option for you if:

SoFi may not be a good option for you if:

Is SoFi legit? Yes, at Financer.com we recommend SoFi.

At Financer.com, all lenders go through a thorough research and review process. We don’t make recommendations lightly.

SoFi is one of the best options out there if you are looking for a large loan with fair rates, zero fees, and flexible repayment terms.

SoFi loans are ideal for borrowers with good credit looking for a huge loan with flexible repayment terms.

SoFi’s APRs are consistent with lenders offering credit to borrowers with excellent credit. They also offer rate discounts for autopayments and all loan rates and terms are disclosed on their website.

What’s more, SoFi offers unemployment protection which means that if you lose your job, your payments may be modified temporarily and the lender may help you find a new job.

Applying for a SoFi loan is an easy and simple process. It’s easy to see if you qualify for a loan without hurting your credit.

Since prequalifying for a SoFi loan only requires a soft credit check, your score won’t be affected until you accept the offer.

SoFi reports to all three credit bureaus.

SoFi doesn’t charge origination, prepayment, or late payment fees. With APRs ranging from 8.99% to 25.81%, SoFi’s rates are consistent with lenders offering credit to borrowers with good to excellent credit.

SoFi also offers discounts for autopayments and all loan rates and terms are disclosed on their website.

SoFi offers repayment terms that range from two to seven years and loans between $5,000 and $100,000. If you are looking for a large loan amount and you have an excellent credit history, SoFi may be the ideal lender.

SoFi has a customer service that runs seven days a week. The lender provides customer support by phone, email, and live chat. SoFi attends to inquiries and complaints Mondays through Thursdays from 5 a.m. to 7 p.m. PT and 5 a.m. to 5 p.m. PT on weekends.

For inquiries or complaints, you can contact SoFi directly at (855) 456-SOFI (7634) or send an email to [email protected].

You can also reach customer support on Twitter at https://twitter.com/SoFi.

Here’s a list of alternatives to SoFi and how they compare:

| Lender | Reviews | Loan Amount | APR | Max. Loan Term | Bad Credit? |

|---|---|---|---|---|---|

| LendKey | View | $5,000 – $300,000 | 4.49-10.68% | Up to 20 years | No |

| Ascent | View | $2,001 – $200,000 | 5.74% to 15.76% | Up to 20 years | Yes |

| Upstart | View | $1,000 to $50,000 | 6.50% – 35.99% | Up to 5 years | Yes |

| Earnest | View | $1,000 to 100% of school cost | 4.79% to 13.50% | Up to 15 years | No |

If you are looking for a large loan and you have good credit, then SoFi is one of the best options out there.

SoFi offers competitive interest rates, especially if you have excellent credit. You’ll also be eligible for a 0.25% rate discount when you set up AutoPay.

SoFi offers attractive perks, zero fees, and no prepayment penalties. What’s more, SoFi’s unemployment protection feature means that if you lose your job, your payments may be modified temporarily and the lender may help you find a new job.

Read more SoFi reviews from customers below or add your own.

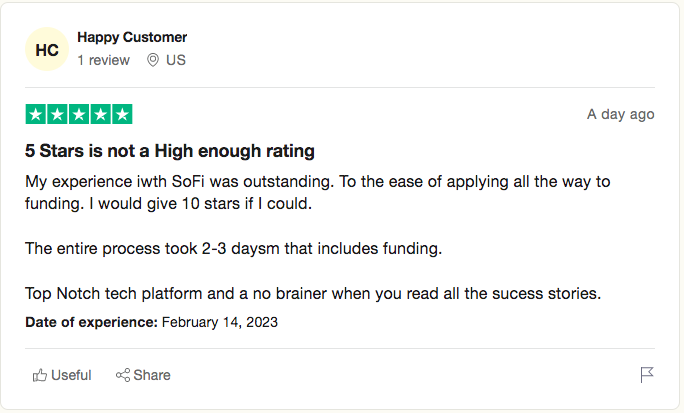

SoFi is rated 4.5 out of 5 stars on Trustpilot, with users generally satisfied with the lender:

Read more reviews on Financer.com from verified users below.

Have you used SoFi before? Leave your review now.

*Disclaimer: Fixed rates from 8.99% APR to 25.81% APR reflect the 0.25% autopay interest rate discount and a 0.25% direct deposit interest rate discount. SoFi rate ranges are current as of 05/19/23 and are subject to change without notice. Not all applicants qualify for the lowest rate. Lowest rates reserved for the most creditworthy borrowers. Your actual rate will be within the range of rates listed and will depend on the term you select, evaluation of your creditworthiness, income, and a variety of other factors. Loan amounts range from $5,000– $100,000. The APR is the cost of credit as a yearly rate and reflects both your interest rate and an origination fee of 0%-6%, which will be deducted from any loan proceeds you receive. Autopay: The SoFi 0.25% autopay interest rate reduction requires you to agree to make monthly principal and interest payments by an automatic monthly deduction from a savings or checking account. The benefit will discontinue and be lost for periods in which you do not pay by automatic deduction from a savings or checking account. Autopay is not required to receive a loan from SoFi. Direct Deposit Discount: To be eligible to potentially receive an additional (0.25%) interest rate reduction for setting up direct deposit with a SoFi Checking and Savings account offered by SoFi Bank, N.A. or eligible cash management account offered by SoFi Securities, LLC (“Direct Deposit Account”), you must have an open Direct Deposit Account within 30 days of the funding of your Loan. Once eligible, you will receive this discount during periods in which you have enabled payroll direct deposits of at least $1,000/month to a Direct Deposit Account in accordance with SoFi’s reasonable procedures and requirements to be determined at SoFi’s sole discretion. This discount will be lost during periods in which SoFi determines you have turned off direct deposits to your Direct Deposit Account. You are not required to enroll in direct deposits to receive a Loan.

Rate & Review SoFi

Your rate for this company. Edit Rate

Take a minute to write a review!

Share your experience and help others to choose the right company.

Pros

Cons

Visit their official website and learn more about SoFi

Or sign in with email

The username or password is incorrect.

Authentication Code:

Borrow up to $20k with Your Premier Lending and get APRs starting at 5.99%.

Thank you for choosing

Share your experience and help others to choose the right company.

This website uses cookies among other user tracking and analytics tools. Cookie information is stored in your browser and performs functions such as recognizing you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful. Cookies may also be used for other marketing and advertising purposes, or for other important business analytics and operations.

To use our website you need to agree to our Terms and Conditions and Privacy Policy. To find more about the legal terms that govern your use of our website, please read our Terms and Conditions here.To find more about your privacy when using our website, and to see a more detailed list for the purpose of our cookies, how we use them and how you may disable them, please read our Privacy Policy here.