Wiki

What Is a Debt-to-Income Ratio? A Complete Guide

- Your DTI ratio divides total monthly debt payments by gross monthly income

- Lenders prefer a DTI below 36%, though some accept up to 43-50%

- A lower DTI improves your chances of loan approval and better interest rates

- You can lower your DTI by paying off debt or increasing income

Adheres to

Adheres to

Reviewed by Ricardo Laizo

Reviewed by Ricardo Laizo6 Min read | Loans

What Is a Debt-to-Income Ratio?

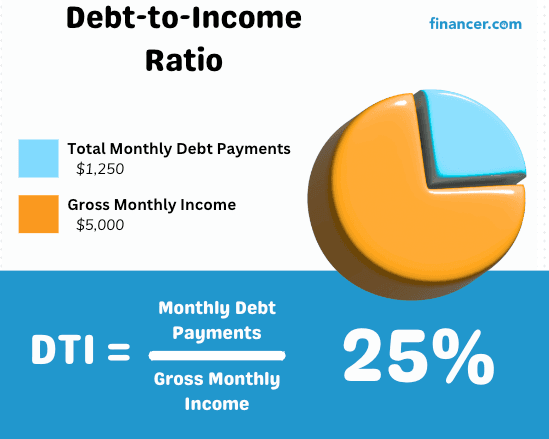

A debt-to-income ratio (DTI) is your total monthly debt payments divided by your gross monthly income, expressed as a percentage. It tells lenders how much of your paycheck is already committed to existing debts.

For example, if you pay $2,000 per month toward debts and earn $6,000 per month before taxes, your DTI ratio is 33%. Lenders use this number to gauge whether you can realistically handle additional monthly payments on a new loan or credit card.

DTI is one of the first things mortgage lenders, auto lenders, and credit card issuers check during an application. A high DTI signals financial strain. A low one suggests you have breathing room in your budget.

Key Takeaway

Aim for a debt-to-income ratio below 36% when applying for loans or credit. A lower DTI gives you stronger approval odds and can help you qualify for better interest rates. If your DTI is above 43%, most conventional lenders will consider you a high-risk borrower.

How to Calculate Your Debt-to-Income Ratio

The debt-to-income ratio formula is straightforward:

DTI = (Total Monthly Debt Payments / Gross Monthly Income) x 100

Here is a quick example. Say you have the following monthly debt payments:

- Mortgage payment: $1,400

- Car loan: $350

- Student loan: $200

- Credit card minimums: $150

Your total monthly debt is $2,100. If your gross monthly income (before taxes) is $6,000, your DTI is:

$2,100 / $6,000 = 0.35, or 35%

That puts you right at the edge of what most lenders consider a healthy ratio.

Step-by-Step DTI Calculation

List All Monthly Debt Payments

Write down every recurring monthly debt payment: credit card minimums, car loan, student loan, mortgage or rent, personal loan payments, child support, and alimony. Only include the monthly payment amount, not the total balance owed.

Tip: Pull up your bank statements or loan accounts to make sure nothing slips through.

Add Up Your Total Monthly Debts

Sum all the monthly payments from step one. For example, if your mortgage is $1,400, car loan is $350, and credit card minimum is $150, your total is $1,900 per month.

Determine Your Gross Monthly Income

Your gross income is what you earn before taxes and deductions. Include your salary, regular bonuses, freelance income, rental income, and any other consistent income sources.

If your income fluctuates (freelancers, gig workers), average your earnings over the past 12 months for a more accurate figure.

Divide and Multiply

Divide your total monthly debts by your gross monthly income. Multiply the result by 100 to get a percentage.

Example: $1,900 / $5,500 = 0.345, or 34.5% DTI.

What Is a Good Debt-to-Income Ratio?

Different DTI ranges send different signals to lenders. Here is how most financial institutions evaluate your ratio:

| DTI Range | Rating | What It Means |

|---|---|---|

| 35% or less | Excellent | You have plenty of income left after debt payments. Lenders view you favorably, and you are likely to qualify for the best rates. |

| 36% to 43% | Manageable | You are carrying a moderate debt load. Most lenders will still approve you, but interest rates may be slightly higher. |

| 44% to 50% | Concerning | You are approaching risky territory. Some lenders may decline your application or require compensating factors like a large down payment. |

| Above 50% | High Risk | More than half your income goes to debt. Loan approval becomes difficult, and it may be time to focus on reducing debt before borrowing more. |

The 43% Rule

For Qualified Mortgages (QM), 43% is generally the maximum DTI a lender can accept under CFPB guidelines. However, some loan programs allow higher ratios with compensating factors like strong cash reserves or a high credit score.

DTI Requirements by Loan Type

Each loan program sets its own DTI ceiling. If your ratio is on the higher side, some programs are more flexible than others:

| Loan Type | Typical Max DTI | Notes |

|---|---|---|

| Conventional (Fannie/Freddie) | 45-50% | Up to 50% with strong compensating factors (high credit score, large reserves) |

| FHA Loans | Up to 57% | Most flexible for borrowers with higher debt loads |

| VA Loans | Up to 60% | No hard cap, but lenders review residual income closely |

| USDA Loans | 41-46% | Front-end ratio capped at 29% |

| Personal Loans | Varies (36-50%) | Online lenders tend to be more flexible than banks |

| Credit Cards | No formal cap | Issuers evaluate DTI but don't publish specific thresholds |

Need some extra cash?

Find the best personal loan in minutes through our comparison. 100% free and easy to use.

Start comparing personal loans now!

Front-End vs. Back-End DTI Ratio

Mortgage lenders look at two types of DTI:

Front-end DTI (housing ratio) includes only housing-related costs: your mortgage payment, property taxes, homeowner's insurance, and HOA fees. Lenders generally want this below 28%.

Back-end DTI (total ratio) includes all monthly debt obligations on top of housing costs: credit cards, car loans, student loans, personal loans, child support, and alimony. This is the number most people refer to when they say "DTI ratio," and lenders typically prefer it below 36%.

When you see a lender reference the "28/36 rule," they mean a front-end ratio of 28% or less and a back-end ratio of 36% or less. This is considered the sweet spot for mortgage qualification.

What Debts Are Included in DTI?

Lenders count all recurring monthly debt obligations when calculating your DTI. Here is what typically gets included:

Debts That Count Toward DTI

Mortgage or rent payments (including property taxes and insurance)

Credit card minimum payments

Auto loan payments

Student loan payments

Personal loan payments

Child support and alimony

Home equity loan or HELOC payments

Any other installment loan payments

What Is NOT Included in DTI

Utilities (electric, water, gas, internet)

Groceries and food expenses

Health insurance premiums

Car insurance

Cell phone bills

Subscriptions and streaming services

Income taxes (your DTI uses gross income, not net)

Income Sources Used in DTI Calculations

Lenders consider all verifiable, recurring income when calculating your DTI:

Pre-tax salary and wages from your primary job

Bonuses and overtime if consistent over the past two years

Self-employment or freelance income (typically averaged over 2 years of tax returns)

Rental income from investment properties (after expenses)

Alimony and child support received

Social Security, pension, and retirement income

Investment dividends if regular and documented

Part-time or second job income if documented for 2+ years

How to Lower Your Debt-to-Income Ratio

If your DTI is too high for the loan you want, you have two levers to pull: reduce your monthly debt payments or increase your income. Here are the most effective strategies:

Pay down credit card balances. Eliminating a $200 monthly minimum payment instantly drops your DTI. Focus on the card with the smallest balance first for quick wins.

Pay off a car loan or personal loan. Removing an installment loan from your obligations makes a big difference, especially if the balance is small enough to pay off before applying.

Avoid taking on new debt. Don't open new credit cards or finance purchases in the months before a major loan application.

Refinance existing loans for lower payments. Extending your loan term or getting a lower rate through debt consolidation can reduce monthly payments.

Increase your income. A raise, side job, or freelance work all count. Lenders want to see at least two years of consistent additional income.

Ask a co-borrower to join the application. Adding a spouse or partner with income but low debt can improve the combined DTI.

Pay down student loans. If you are on an income-driven repayment plan with low payments, lenders still use the actual payment. Paying off small student loans removes them from the equation.

Does DTI Affect Your Credit Score?

Your debt-to-income ratio does not directly affect your FICO credit score. Credit bureaus don't have access to your income information, so DTI is not part of the scoring model.

That said, DTI and your credit score are related in practice. High debt levels often go hand-in-hand with high credit utilization (the percentage of your available credit you are using), which does affect your score. The credit utilization ratio is the second-biggest factor in your FICO score after payment history.

Think of it this way: your credit score tells lenders how reliably you pay your debts. Your DTI tells them whether you can afford to take on more.

DTI Ratio Examples at Different Income Levels

Here is how DTI works out at various salary levels, so you can see where you might land:

| Annual Income | Gross Monthly Income | Max Debt at 36% DTI | Max Debt at 43% DTI |

|---|---|---|---|

| $40,000 | $3,333 | $1,200 | $1,433 |

| $60,000 | $5,000 | $1,800 | $2,150 |

| $80,000 | $6,667 | $2,400 | $2,867 |

| $100,000 | $8,333 | $3,000 | $3,583 |

| $120,000 | $10,000 | $3,600 | $4,300 |

What Happens If My DTI Is Too High?

A DTI above 43% does not automatically disqualify you from borrowing, but it does narrow your options.

With a high DTI, you may face higher interest rates on any loan you qualify for. Some lenders will decline your application outright. Others may approve you but with stricter conditions, like a larger down payment or a co-signer.

For mortgages specifically, government-backed programs like FHA loans tend to be more flexible, accepting DTIs up to 57% with compensating factors. VA loans can go even higher if your residual income is strong.

If you are struggling with high debt, consider exploring debt consolidation or creating a payoff plan with our guide on how to get out of debt.

Frequently Asked Questions

What is a good debt-to-income ratio?

What is a good debt-to-income ratio?

A DTI of 36% or below is considered good by most lenders. Some mortgage programs accept ratios up to 43-50%, but you will generally get better rates and terms with a lower ratio.

How do I calculate my debt-to-income ratio?

Add up all your monthly debt payments (mortgage, car loan, student loans, credit card minimums, etc.) and divide by your gross monthly income. Multiply by 100 to get a percentage. For example, $2,000 in monthly debts divided by $6,000 gross income equals a 33% DTI.

Does rent count in debt-to-income ratio?

Yes. If you are renting, your monthly rent payment is included in your DTI calculation. If you are applying for a mortgage, lenders will replace your rent with the projected mortgage payment (including taxes and insurance) to calculate your future DTI.

What is the maximum DTI for a mortgage?

It depends on the loan type. Conventional loans typically cap at 45-50%, FHA loans allow up to 57%, and VA loans can go up to 60%. The standard Qualified Mortgage threshold is 43%, but many programs have exceptions for strong borrowers.

How can I lower my debt-to-income ratio?

You can lower your DTI by paying off existing debts (start with small balances), avoiding new debt before applying for a loan, increasing your income, refinancing existing loans for lower monthly payments, or consolidating debt.

Does DTI affect my credit score?

No, your DTI does not directly impact your credit score because credit bureaus do not have access to your income data. However, high debt levels often correlate with high credit utilization, which does affect your score.

Should I use gross or net income to calculate DTI?

Use gross income (before taxes and deductions). This is the standard that lenders use. Calculating with net income would give you a higher DTI than what lenders actually see.

What are common DTI mistakes?

The most common mistakes include forgetting to count co-signed loan payments, using net income instead of gross income, leaving out small debts like medical payment plans, and not including projected payments on a new loan you are applying for.

Comments

Only registered users can leave comments.