What is Loan Amortization?

Certain financial terms can often feel like they’re designed to confuse rather than clarify. Amortization is one such term.

In the most basic sense, amortization is the process of spreading out a loan into a series of fixed payments over time.

These payments are structured so that you’re paying off both the interest and the principal (the original amount borrowed) gradually.

Loan Amortization In a Nutshell:

Loan Amortization is the process of spreading out a loan into a series of fixed payments over time. When you take out an amortizing loan, each payment you make consists of two main parts: the principal and the interest.Principal and Interest

- Principal: This is the original amount of money borrowed.

- Interest: This is the cost of borrowing the principal, usually expressed as a percentage rate.

The Amortization Schedule

An amortization schedule is a table detailing each periodic payment on an amortizing loan. This schedule is characterized by:- Decreasing Interest Payments: Early in the schedule, a larger portion of each payment is devoted to interest.

- Increasing Principal Reduction: Over time, a larger portion of each payment goes towards reducing the principal.

Calculating Amortization Involves:

- Loan Amount: The total amount borrowed.

- Interest Rate: Usually an annual rate, but payments are often monthly.

- Loan Term: The duration over which the loan is to be repaid.

Benefits of Amortization

- Predictability: Borrowers know exactly how much they need to pay each period.

- Interest Savings: As the principal decreases, the interest accrued decreases, leading to potential savings over the life of the loan.

Considerations

- Early Payments: Paying more than the scheduled payment can reduce the loan balance faster, saving on interest.

- Refinancing: Changing the terms of your loan can affect the amortization schedule.

The Amortization Schedule: Your Loan Roadmap

The real heart of amortization is the amortization schedule. This is a table detailing each payment throughout the life of the loan. It shows:

- The total payment amount.

- How much of each payment goes towards the interest.

- How much is applied to the principal.

- The remaining balance after each payment.

In the early stages of your loan, a larger portion of your payment is devoted to interest. As time goes on, this shifts, and more of your payment goes towards reducing the principal.

Why Does Front-Loaded Interest Matter?

This front-loaded interest structure has some implications:

- Equity Building: In the early years of a loan, you’re building equity at a slower pace. This is crucial to understand, especially for those who might consider selling their asset (like a house) within a few years of purchase.

- Refinancing Considerations: If you’re contemplating refinancing, it’s essential to understand where you are in your amortization schedule. Refinancing early in the term might mean you’re restarting the cycle of high-interest payments.

- Prepayment Benefits: Making extra payments towards the principal early in the loan can significantly reduce the total interest you pay over the life of the loan.

Different Types of Amortization

Amortization can vary in structure depending on the type of loan and the specific terms agreed upon between the borrower and lender.

Understanding these different types of amortization is crucial for borrowers, as it affects how payments are calculated and the overall cost of the loan.

| Type of Amortization | Impact on Borrower | Payment Progression | Risks/Benefits |

|---|---|---|---|

| Annuity Amortization | Fixed payment amount, easy budgeting | Starts with higher interest, transitions to higher principal | Predictable payments; more interest paid initially |

| Straight-Line Amortization | Consistent principal repayment | Decreasing total payment as interest reduces | Easy to track principal reduction; potentially higher initial payments |

| Declining Balance Amortization | Decreasing payment amount over time | Starts high, reduces as loan matures | Lower payments later in loan term; higher initial financial burden |

| Balloon Payment Amortization | Lower payments until term end | Consistent payments followed by one large payment | Risk of large end payment; refinancing may be necessary |

| Negative Amortization | Initially lower payments, increasing balance | Payment less than interest; balance grows | Can lead to increased debt; careful management required |

| Interest-Only Amortization | Interest payments only initially | Only interest initially, then switches to include principal | Lower initial payments; higher payments later |

Annuity Amortization: The Standard for Mortgages

The most popular type of amortization for mortgages is the Annuity Amortization. This method is also commonly referred to as the “traditional” or “standard” amortization schedule. Here’s why it’s widely used:

- Fixed Payments: Annuity amortization schedules involve fixed payments over the term of the loan. This means that borrowers pay the same amount every month, which helps in budgeting and financial planning.

- Composition of Payments: In the early years of the mortgage, a larger portion of each payment goes towards paying interest. As time progresses, a greater portion of the payment is applied to the principal. This is because the interest is calculated on the remaining principal, which decreases with each payment.

- Predictability and Stability: This method provides a predictable and stable payment structure, which is particularly appealing for residential mortgages. Homeowners appreciate knowing exactly what their payments will be for the life of the loan, without worrying about payment amounts changing.

- Full Amortization: These loans are fully amortized, meaning that if all payments are made as scheduled, the loan will be completely paid off at the end of the term. There is no balloon payment or lump sum due at the end.

- Flexibility in Terms: Mortgages with annuity amortization can come in various term lengths, such as 15, 20, 30, or even 40 years, providing flexibility for borrowers to choose a term that best fits their financial situation.

- Widespread Availability: This type of amortization is the standard in the industry, offered by most lenders for residential mortgages. It’s well-understood, highly regulated, and comes with various consumer protection features.

Read More: Mortgage Amortization: Straight-Line vs. Mortgage-Style

Straight-Line (Linear) Amortization

- Characteristics: In straight-line amortization, the principal payment remains constant throughout the term of the loan. The interest payment decreases over time as the principal balance reduces.

- Common Usage: This method is often used in personal loans and some types of business loans.

Declining Balance Amortization

- Characteristics: Payments are larger at the beginning of the loan term and gradually decrease over time. The decrease is due to the interest being calculated on a declining principal balance.

- Common Usage: This method is less common but can be found in some types of installment loans or business loans.

Balloon Payment Amortization

- Characteristics: In this type, regular payments of interest and possibly some principal are made for a set period, followed by a large ‘balloon’ payment at the end of the loan term. This final payment covers the remaining principal balance.

- Common Usage: Often used in commercial real estate loans and some types of personal loans.

Negative Amortization

- Characteristics: This occurs when the loan payments are set below the amount needed to cover the interest cost. As a result, the unpaid interest is added to the principal balance, causing the loan balance to increase over time rather than decrease.

- Common Usage: It’s found in some adjustable-rate mortgages but is generally considered risky for borrowers.

Interest-Only Amortization

- Characteristics: In this structure, borrowers pay only the interest on the loan for a certain period. After this phase, the loan typically converts to a standard amortizing loan, where payments include both principal and interest.

- Common Usage: This is often used in certain types of mortgages and investment loans.

Amortization Calculations Explained

Understanding amortization calculations is essential for any borrower, as it provides insight into how loan payments are allocated towards principal and interest over the life of the loan.

But rather than pulling out your own calculator, click here to leverage our loan amortization calculator, which simplifies this process significantly. Here’s a brief overview of how these calculations work and how our calculator can assist you.

Essential Components of Amortization Calculations

- Loan Amount: The initial sum borrowed.

- Interest Rate: The rate at which interest is charged on the loan, usually an annual rate but calculated monthly.

- Loan Term: The duration over which the loan will be repaid, often in years.

The Amortization Formula

To calculate monthly payments for a fixed-rate loan, we use a specific formula that considers the principal, interest rate, and loan term:

Here, P represents the principal, r is the monthly interest rate, and n is the total number of payments.

Simplifying Calculations with Our Calculator

Our loan calculator streamlines this process:

- Input the Loan Details: Enter the total loan amount, annual interest rate, and loan term in years.

- Automatic Calculation: The calculator automatically converts the annual interest rate to a monthly rate and determines the total number of payments.

- Instant Breakdown: It then applies the amortization formula and provides you with the monthly payment amount, alongside a detailed breakdown of how much goes towards the principal and interest.

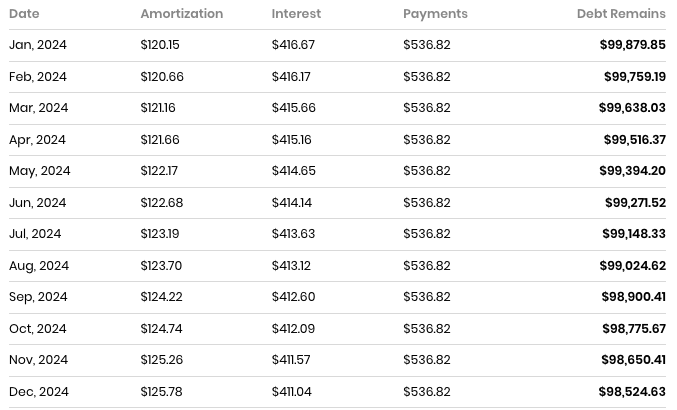

Visualizing with an Amortization Schedule

The calculator also generates an amortization schedule, offering a clear view of how each payment is divided over the loan term.

This schedule is particularly helpful in visualizing the shift from primarily interest-focused payments to principal-focused payments as the loan matures.

How to save $435.00 on your loan

The price difference for a $500.00 loan in 90 days is $435.00.

What You Need to Know About Amortization

When navigating the waters of loan amortization, borrowers often focus on the surface details — monthly payments and interest rates.

However, truly understanding the concept of amortization reveals strategic opportunities that can have a significant impact on one’s financial journey. Here’s an insightful perspective on amortization that every savvy borrower should consider.

Equity Building vs. Interest: The Early Years’ Trade-off

The initial stage of an amortized loan is skewed towards interest payments. This structure often surprises borrowers, as they see their principal balance decrease only marginally despite regular payments.

Understanding this front-loaded interest phenomenon is key to making informed financial decisions, such as the potential benefits of making additional principal payments early in the loan term to accelerate equity building and reduce total interest paid.

Expert Tip: Reconsider the “Starter Home” Strategy

The Power of Prepayments

One of the most impactful strategies in loan amortization is making prepayments. Even small additional amounts towards the principal can shorten the loan term and cut down the total interest significantly.

Borrowers should use amortization schedules to forecast the effects of additional payments and consult with their lender about any potential prepayment penalties.

Refinancing: A Double-Edged Sword

Refinancing can seem like a beacon of relief when interest rates drop, offering lower monthly payments or a shorter loan term. However, it’s essential to consider the reset of the amortization schedule that accompanies refinancing.

A new loan means that payments are once again applied more heavily towards interest. Calculating the break-even point and long-term cost implications is a must before taking this step.

Read More: How to Refinance a Personal Loan: 7 Easy Steps

Adjustable-Rate Mortgages (ARMs) and Amortization

ARMs add a layer of complexity to amortization. Initially, these loans may offer lower payments, but as interest rates fluctuate, so will the payments and the loan’s amortization schedule.

Borrowers with ARMs should be financially prepared for the possibility of increased payments and a changing amortization timeline.

Amortization in Investment Properties

For investment property owners, amortization holds additional implications, particularly when it comes to taxes. The ability to deduct mortgage interest can be a significant financial benefit.

Additionally, understanding how amortization affects cash flow and the return on investment for rental properties is critical for long-term financial planning.

The Long-Term Perspective

Amortization schedules are not just a monthly roadmap; they are a long-term financial planning tool. Borrowers should periodically review their amortization schedule alongside their financial goals.

Life changes — such as income fluctuations, changes in family dynamics, or shifts in the housing market — may warrant a reassessment of one’s loan strategy.

FAQs about Amortization

What exactly is amortization?

Amortization is the process of paying off a debt over time through regular payments. A part of each payment goes towards the interest, and the remaining amount reduces the principal balance.

How does an amortization schedule work?

An amortization schedule outlines each payment on a loan over time, showing how much goes towards interest and how much goes towards reducing the principal. Initially, payments are mostly interest, but over time more of your payment goes to the principal.

Why do early payments mostly go toward interest?

Lenders calculate interest based on the remaining balance of the loan. In the early stages of repayment, the principal balance is highest, so the interest portion of the payment is greater.

Can I save money by making extra payments on my loan?

Yes, making additional payments towards the principal can reduce the total amount of interest paid over the life of the loan and can potentially shorten the loan term.

Does refinancing affect amortization?

Refinancing can reset the amortization schedule, often resulting in a return to payments that are predominantly interest. It’s important to calculate whether refinancing will offer a true cost benefit over the course of the loan.

Are there different types of amortization for different loans?

Yes, there are several types of amortization, including straight-line (linear), declining balance, balloon payment, negative amortization, and interest-only, each with unique payment structures and implications.

What type of amortization is most common for mortgages?

The most common type for mortgages is annuity amortization, where payments are fixed over the term and gradually shift from being interest-focused to principal-focused.

How can I calculate my monthly loan payment?

Monthly loan payments can be calculated using the amortization formula, which factors in the loan amount, interest rate, and term of the loan. Alternatively, you can use online calculators to simplify this process.

Is it better to have a shorter or longer amortization period?

This depends on your financial situation. A shorter amortization period means higher monthly payments but less interest over time. A longer amortization period reduces monthly payments but increases the total interest paid.

How does amortization affect my taxes?

For some loans, like certain mortgages, the interest part of the payment may be tax-deductible. The implications vary widely based on local tax laws and the loan type, so consult a tax professional for advice specific to your situation.

Can I change my amortization schedule?

Yes, you can change your amortization schedule by refinancing the loan, making extra payments, or adjusting the terms with your lender. However, each of these options may have financial implications that should be considered carefully.